Jumbo loan debtors typically require to have about 6 months' worth of payments in their checking account after they close on your home; that dramatically contrasts with traditional borrowers, who just require about 2 months' worth of home loan payments set aside. Jumbo loans may not be appropriate for everybody, but they do have some outrageous advantages.

Even more, interest on the loans valued at approximately $1 million is tax-deductible, which can provide a huge boon for big-time customers. Financial professionals at Tucker Home loan might be able to help you determine whether you get approved for these high-end loans. Now that we have covered the more conventional kinds of loans, let's depart into the more complex world of variable-rate mortgages, which can trigger some confusion among borrowers.

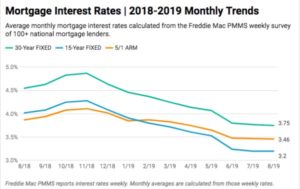

Unlike fixed-rate mortgages, these loans involve rates of interest adjustments in time. ARMs are considered riskier loans due to the fact that the rates of interest is likely to increase as the regard to the loan progresses. The majority of ARMs are developed on a 30-year mortgage plan. Borrowers choose their initial term, throughout which an introductory rate is used.

You would then pay the adjusting rate for twenty years. All of the ARMs are based off of a 30-year terms - who took over abn amro mortgages. For a 7/1 ARM, you would pay the initial rate for seven years, and after that you would have a rate that continuously adjusts for 23 years. Likewise, introductory rates last for five years with a 5/1 home mortgage and 3 years for a 3/1 ARM.

The 10-Second Trick For What Do I Need To Know About Mortgages And Rates

Your loan imitates a fixed-rate home loan throughout the initial term. Then, after the initial period, your loan ends up being tied to a rates of interest index. That implies that your loan rate can change by a number of points every year; it is periodically re-evaluated after the initial duration ends. The rates of interest indexes can come from a number of sources.

Your rates of interest might change, however there will be a designated annual cap to http://titusgtxp766.unblog.fr/2020/10/11/what-does-what-is-the-harp-program-for-mortgages-mean/ prevent a frustrating walking in your rates of interest in a brief time period. Still, the very first change after your lower-rate introductory duration may be a shock, due to the fact that these limits do not constantly apply to that initial modification.

That is why financial professionals at Tucker Home loan recommend the ARM loan for individuals who intend to remain in their houses for only a short time. If you think you will be leaving the home within a five-year window, it might make more sense to conserve cash on your regular monthly payments by enjoying a lower rate and then offering your home before the interest amount is adjusted.

This is why ARMs are usually thought about riskier, however they can be helpful for short-term purchasers. For those who desire an even lower payment at the beginning of their ARM, the interest-only 5/1 and 3/1 might be the perfect alternative. Interest-only loans indicate that you are only paying interest throughout the very first 3- or five-year period.

Examine This Report about What Banks Give Mortgages Without Tax Returns

The home loan's principal is not being paid for at all; during the introductory duration, you are just paying interest on the loan. Who would benefit from this type of arrangement? The majority of professionals say that the very best prospect for an interest-only loan is somebody who means to settle the loan completely before the interest-only duration ends.

Borrowers can constantly pick to re-finance an interest-only or traditional ARM, however this can be a potentially expensive relocation, thinking about the countless dollars required to finish the process. It is very important to weigh the benefits of an ARM over the fixed-rate option, thinking about that the ARM may eventually cost more over the long term.

USDA loans are developed to assist low-income Americans purchase, repair work and renovate homes in backwoods of the nation. In order to get approved for this kind of loan, the debtor must have an income that falls between 50 and 80 percent of the area's median earnings; in other words, they are usually thought about low-income borrowers.

Homes bought through this program must be thought about "modest" for the area, and they likewise have to meet a shopping list of other requirements. Low-income debtors who are thinking about buying a rural home should consult their loan providers to find out more about the USDA aids and loan programs. Loans through the VA are just readily available to those who have served in the military, consisting of the National Guard and Reserve.

How What Happened To Cashcall Mortgage's No Closing Cost Mortgages can Save You Time, Stress, and Money.

There are a range of service limitations that must be met in order for the customer to be eligible, as well. For example, any veteran who has actually been serving from 1990 to the present need to have served for 24 continuous months, among other requirements. National Guard and Reserve members must have served for at least 6 years before being put on the retired list, receiving a respectable discharge or being moved to a Standby or Ready Reserve unit.

Specialists at Tucker Home mortgage might have the ability to assist veterans find out more about their eligibility for these unique loans. As you can see, there are a variety of home mortgage options that may be offered to debtors throughout the home-buying process. It is important to thoroughly consider your financial scenario and job your desired future payments prior to committing to a mortgage.

Even a risky loan might be appropriate for your personal situation, depending upon your needs and plans! Do not mark down any of the loans just because they offer a non-traditional format. Consult a home loan expert to identify which mortgage is ideal for you!Qualifications for all of IHCDA's homebuyer programs are identified by your overall home earnings being under the program earnings limitation for the county you are purchasing your home in.

A debtor can likewise receive 3-4% down payment help, depending on the type of loan funding, based off of the list prices of the house being acquired. The help comes in the type of a second home mortgage, however brings no interest and no payments. The down payment assistance funds should be repaid completely if the customer selects to re-finance or sell in the very first two years of owning the house.

Fascination About What Were The Regulatory Consequences Of Bundling Mortgages

If you're purchasing a house, chances are you need to be purchasing home loan as welland nowadays, it's by no implies a one-mortgage-fits-all model. Where you live, how long you plan to remain put, and other variables can ensure home mortgage loans better matched to a home buyer's circumstances and loan quantity.

Lots of types of mortgage loans exist: traditional loans, FHA loans, VA loans, fixed-rate loans, variable-rate mortgages, jumbo loans, and more. Each home loan may require certain down payments or specify requirements for loan amount, mortgage insurance coverage, and interest. To find out about all your home-buying choices, examine out these common kinds of house mortgage loans and whom they're suited for, so you can make the best choice.

The most common kind of conventional loan, a fixed-rate loan recommends a single interest rateand monthly paymentfor the life of the loan, which is typically 15 or 30 years. One kind of fixed-rate mortgage is a jumbo loan. House owners who long for predictability and aren't going anywhere soon may be finest matched for this conventional loan.